By Paul Frimpong

Let’s not pretend that we aren’t worried about the current global economic happenings that have thrown all predictions into disarray.

By this, I am referring to the decline in global economic growth; the rise of public debt above sustainable levels across major economies, especially in emerging markets; the degree of decay when it comes to public health due to the COVID-19 pandemic; and now the Russia-Ukraine war and its attendant consequences.

In all these uncertainties and global risks, no single country is an exception, as that’s the case for Ghana.

In this article, first originally written for and published by Ghana Invest, a Paris-based private diaspora-led organization dedicated to the promotion of Ghanaian trade, industry and investment abroad, I will be sharing some insights, which border on Ghana’s quest for economic recovery, which could be shorter or longer, depending on the approach that the government of the day chooses.

Foreign direct investment (FDI) is an integral part of an open and effective international economic system and a major catalyst for development.

The question is, how will Ghana catalyse FDI for its economic recovery?

Economic Outlook

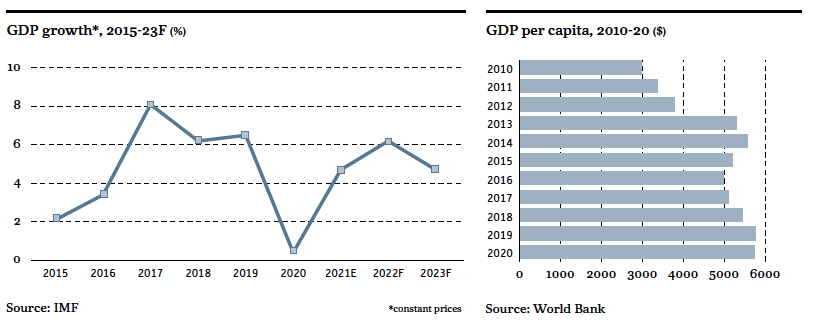

According to a recent IMF report, Ghana’s economy is projected to remain relatively strong over the medium term, supported by higher prices for key exports and strong domestic demand. Growth is projected to reach 5.5% in 2022 and average 5.3% over 2022. Growth is expected to be broad-based, led by agriculture and services, and a relatively stronger industry sector.

‘Light at the end of the tunnel’

Let me make it simple for you to grasp. Ghana’s current economic situation fits the phrase, “There’s light at the end of the tunnel.”

In the wake of the recent COVID-19 outbreak, global commodity price fluctuations, and the instabilities and uncertainties in and around Europe, the Ghanaian economy has suffered a great deal of economic difficulties at the macro and micro levels.

The war in Ukraine is expected to exacerbate already-existing fiscal and macroeconomic challenges, slowing growth to pre-pandemic levels.

The developments are expected to raise global prices for a number of key commodities, including food, fuels, fertilizers, and metals used in manufacturing, adding to Ghana’s already-existing inflationary pressures.

However, one could argue that the road to recovery could be shorter than anticipated if governments had the political will to stay through on the fiscal discipline that’s required in times like these.

Rising debt levels

Ghana’s public debt has risen past the sustainable levels for an emerging economy. The country’s current debt is over 80% of its GDP.

The overall fiscal deficit doubled to 15.2% in 2020 and public debt increased to 81.1% in 2020, placing Ghana at a significant risk of debt distress.

These rising public expenditures in the context of persistently weak revenue performance have undermined Ghana’s fiscal and debt sustainability in recent years. As the country’s fiscal risks remained high, credible fiscal consolidation was required to reverse the unfavourable debt dynamics and reduce domestic refinancing risks.

Home-grown policies

In the wake of these fiscal management challenges, the government has developed and introduced policy measures and programs aimed at restoring fiscal discipline, reversing the fiscal deterioration, and putting the public debt on a downward and sustainable path.

The government’s 2022 budget sets forth an ambitious consolidation plan as it aims to raise revenue from 16% in 2021 to 20% in 2022. Fiscal measures would reduce the deficit from 12% in 2021 to 4.5% by 2024.

E-Levy

In a move to stimulate domestic revenue growth, which is ideal in this situation looking at the impossible state for the country to borrow from the international capital market, the government has introduced an electronic transfer levy, which has faced steep opposition from the Ghanaian populace.

The E-levy is estimated to generate 1.4% of 2022 GDP.

Catalysing on FDI for quicker recovery

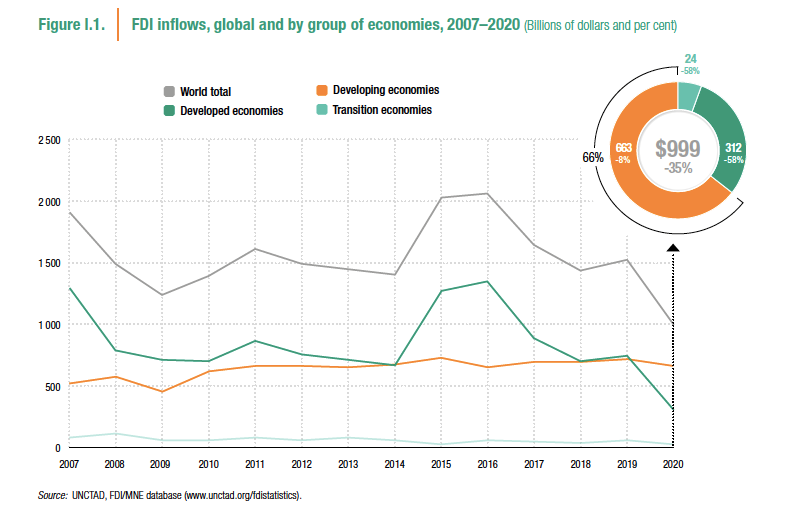

Global FDI flows fell by 35% in 2020, reaching $1 trillion from $1.5 trillion in 2019.This is the lowest level since 2005 and nearly 20% lower than the post-global financial crisis trough in 2009.

Greenfield investments in industry and new infrastructure investment projects in developing countries were hit especially hard. This is according to the World Investment Report, 2021.

Among developed countries, FDI flows to Europe fell by 80 percent. The fall was magnified by large swings in conduit flows, but most large economies in the region saw sizeable declines. Flows to North America fell by 42%, while those to other developed economies fell by about 20% on average.In the United States, the decline was mostly caused by a fall in reinvested earnings.

FDI flows to Africa fell by 16% to $40 billion, a level not seen in 15 years. Greenfield project announcements, the key to industrialization prospects in the region, fell by 62 per cent. Commodity exporting economies were the worst affected.

Flows to developing Asia were resilient. In fact, inflows into China increased by 6% to $149 billion. South-East Asia saw a 25% drop, with its reliance on GVC-intensive FDI playing a significant role. FDI flows to India increased, driven in part by M & A activity.

Now that we have had a fair idea of the FDI flows globally and in specific regions, let’s zero in now on Ghana, which is our point of focus.

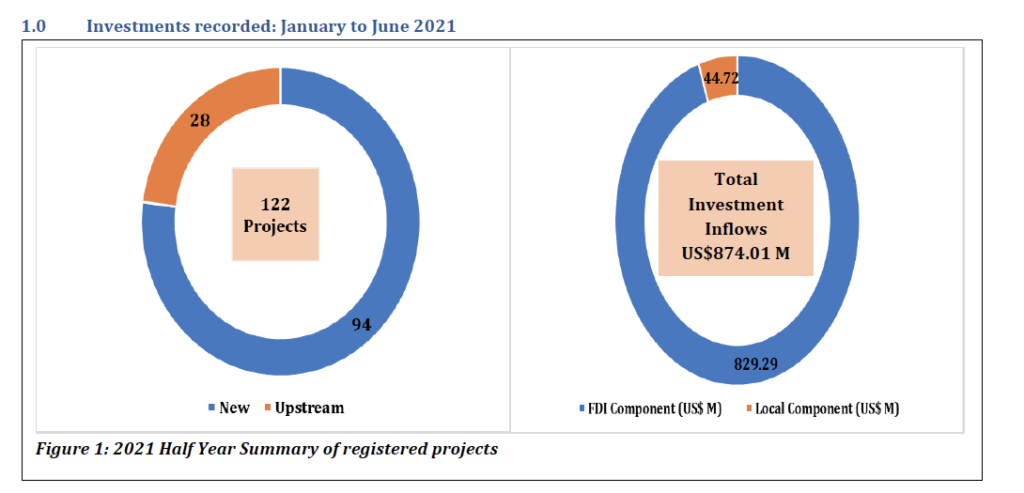

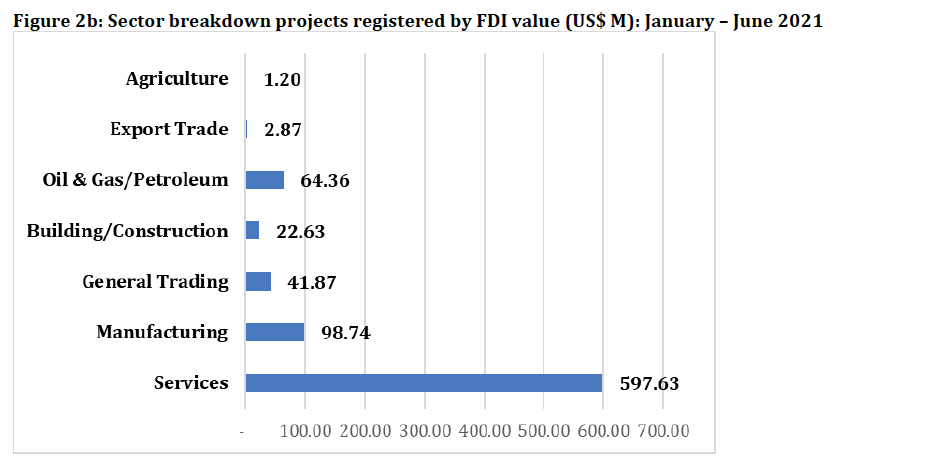

In a quarterly briefing report by the Ghana Investment Promotion Centre (GIPC), between “January to June 2021, Ghana recorded 122 projects with a total estimated investment of US $874.01 million.

The FDI component and the local components amounted to US $829.29 million and US $44.72 million, respectively, for the first half of 2021. The FDI value of US $829.29 million represents an increase of 32.15% over the FDI value of US $627.52 million recorded in the first half of 2020. The total initial capital transfers also amounted to US $47.76 million for the first half of 2021.

Source: GIPC Quarterly Investment Report, 2021

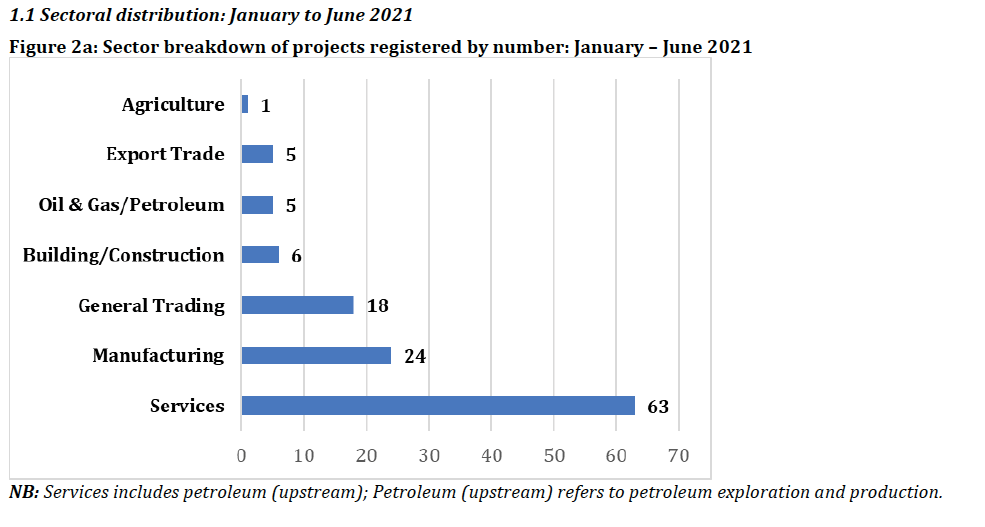

The services sector recorded the highest number of projects at 63, followed by the manufacturing sector, which recorded 24 projects, as seen in the figure below.

The services sector, of course, due to the volumes in the project numbers, recorded the largest value in terms of FDI of US$597.63 million followed by the manufacturing sector with an FDI value of US$98.74 million.

While the international investment architecture is an important driver of FDI flows, national policies play an important role as well.

As most studies have revealed and as is evident across multiple economies, FDI triggers technology spillovers, assists human capital formation, contributes to international trade integration, helps create a more competitive business environment, and enhances enterprise development.

It differs from other major types of external private capital flows in that it is primarily motivated by the investors’ long-term prospects for profit in production activities over which they have direct control.

For a country like Ghana, the case is no different in how FDI could become a catalyst for economic recovery. It has already proven to become an important source of private external finance.

Given the scale and magnitude of the opportunities that could be leveraged from FDI, it has become imperative that Ghana develop a coherent policy approach to establish a hospitable regulatory framework for FDI.

These issues border on rules regarding market entry, foreign ownership, and treatment accorded to foreign-owned firms, as well as improving the general market functions.

They also include a conscious approach to including investment promotions, investment incentives (tax, etc.), post-investment services, amenity improvements, and measures to reduce the cost of doing business.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}