In the face of rising prices of precious metals, declining ore grades and rising extraction complexity, operational costs are elevating industry-wide, pressuring margins and forcing capital shifts toward innovation and efficiency. On the other hand, automation, robotics and digital transformation are becoming core competitive factors, towards improving safety and efficiency.

Early in the year, global mining markets are bracing up for the fallouts of a potential $200 billion merger between Rio Tinto and Glencore. The merger could face Chinese regulatory hurdles over the expected dominance of a combined Rio Tinto – Glencore entity in the copper and iron ore markets.

In Ghana, the Abosso Gold Fields, Damang mine is expected to be in the late stages of its transition to Government ownership ahead of a full handover, with operations largely focused on processing remaining stockpiles rather than fresh ore, pointing to subdued output and tighter margins versus historical levels. A supportive gold price environment (around US$5,000 per ounce) during the year should provide partial revenue support with the near-term outlook shaped by lower throughput and ongoing feasibility work to assess post-handover redevelopment options and potential life-of-mine extension.

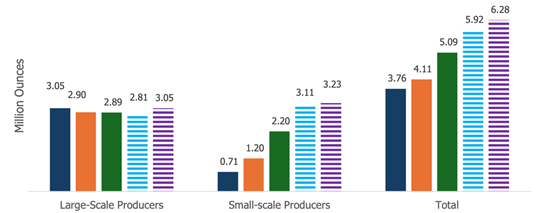

Building on the latest production trend, gold is expected to further entrench its role as the anchor of Ghana’s mining sector, with total output increasing from 5.1 million ounces in 2024 to approximately 6.3 million ounces by 2026. Growth is overwhelmingly driven by the small-scale segment, which expands more than fourfold from about 0.7 million ounces in 2022 to over 3.2 million ounces by 2026, raising its share of national production to just above 50%. In contrast, large-scale producers are projected to remain broadly stable, easing from around 3.0 million ounces in 2022 to a trough near 2.8 million ounces in 2025 before recovering to roughly 3.0 million ounces in 2026. This evolving production mix underscores the need for continued formalization, stronger regulatory oversight, and enhanced governance frameworks to support environmental compliance while improving the state’s capacity to deepen royalty capture and strengthen sector resilience.

Chart 1.5: Gold Production in Ghana by Producer Type (2022–2026)

ECONOMIC AND MARKET OUTLOOK, AND STRATEGIC INVESTMENT ORIENTATION FOR 2026

Source: Minerals Commission, MIIF

The commodities market enters 2026 amid persistent geopolitical risk, uneven global growth, and ongoing structural shifts tied to the energy transition and supply chain realignment. Bloomberg consensus points to a largely range-bound pricing environment rather than a broad cyclical upswing.

Precious metals are expected to remain a core hedge within the complex. Gold is projected to rise to US$5,750/oz in Q1 before easing to US$4,865/oz in Q2, followed by a renewed rally toward US$5,308/oz in Q4. This outlook reflects continued support from geopolitical risk, sustained central bank demand, and expectations of softer real interest rates, alongside some degree of price normalization later in the year. Silver is expected to display moderate volatility, increasing from US$120.00/oz in Q1, adjusting to US$100.00/oz in Q2, and advancing to US$108.00/oz by Q4, driven by its combined exposure to investment flows and industrial demand.

In battery materials, Lithium SC prices are projected to firm gradually, rising from a median of US$2,375/mt in Q1 2026 to US$2,600/mt by Q4 2026, before extending gains toward US$2,800/mt in Q1 2027. This trajectory points to a market that is steadily rebalancing as demand from the battery supply chain improves, while ongoing project ramp-ups and residual inventories continue to temper the pace of recovery.

Brent crude oil price projections indicate a decline from an average of US$68/bbl in 2025 to around US$60/bbl in 2026, marking a five-year low. The expected softening reflects slower demand growth, driven by the rising adoption of electric and hybrid vehicles and signs of stagnating oil consumption in China. Notwithstanding this baseline outlook,

elevated geopolitical risks present a material upside risk to prices and could trigger periods of heightened volatility.

Chart 1.6: Price Forecasts for Key Metals (Consensus Median Price)

Source: Bloomberg, MIIF

Meanwhile, the rapid expansion of AI and growing electricity demand to power data centers could raise prices for energy and for base metals like aluminum and copper, which are essential for electricity generation and AI infrastructure.

ECONOMIC AND MARKET OUTLOOK, AND STRATEGIC INVESTMENT ORIENTATION FOR 2026

. Equities Outlook

The global equities market is expected to sustain its positive momentum in 2026 and over the medium term, with forecast returns ranging between 9% and 12%, supported by resilient corporate earnings and steady economic growth across regions. The International Monetary Fund (IMF) projects global economic growth of 3.1% in 2026, which is expected to underpin equity market performance. While elevated government deficits remain a potential risk to the global outlook, diversification across sectors is likely to continue supporting earnings expansion.

An additional driver of equity returns in 2026 is the anticipated continuation of monetary easing by central banks as inflation moderates. Lower interest rates are expected to stimulate business activity, support consumer spending, and enhance equity valuations. In the United States, the S&P 500 is projected to rise by 12% according to Goldman Sachs, while equity markets in Europe and Japan are also expected to record positive returns.

Debate surrounding technology stock valuations persists as capital expenditure on artificial intelligence (AI) remains elevated. However, analysts generally argue that recent rallies in large technology stocks are driven more by earnings prospects and productivity gains than by speculative excesses linked to AI.

On the domestic front, trading activity on the Ghana Stock Exchange (GSE) is expected to be concentrated in ICT, Food and Beverages, and financial stocks in terms of both volumes and values. The GSE Composite Index (GSE-CI) is projected to return approximately 81%, supported by commodity-linked equities, while the GSE Financial Stock Index (GSE-FSI) is forecast to deliver returns of about 95% over the same period.

Overall, the combination of declining interest rates and inflation, improving corporate profitability, sustained investment in AI, and continued economic expansion presents favorable conditions for equity market appreciation in 2026.

Fixed Income Outlook

The global fixed-income environment in 2026 is expected to be characterized by policy stabilization rather than aggressive easing, as inflation moderates while economic growth remains relatively resilient. According to the IMF’s January 2026 World Economic Outlook Update, global growth is projected at about 3.3%, with major central banks expected to proceed cautiously. The U.S. Federal Reserve is likely to keep its policy rate broadly within the 3.50%-3.75% range, with any rate cuts more likely to occur later in the year and to be modest in scale. Similarly, the European Central Bank has signaled no urgency to adjust policy, with its deposit rate expected to remain around 2.0% for an extended period as inflation converges gradually toward target. In this context, longer-term global bond yields, including the U.S. 10-year Treasury, are expected to trade within a relatively stable 3.5%-4.0% range, supporting steady capital flows to emerging and frontier markets rather than a sharp global bond rally.

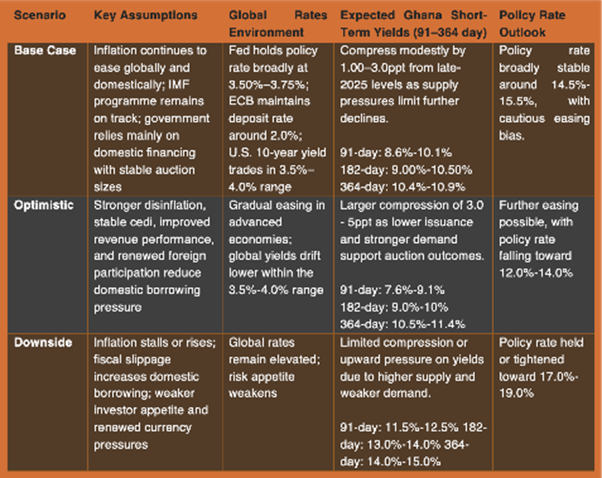

Against this backdrop, Ghana’s fixed-income outlook for 2026 remains cautiously constructive, supported by improved macroeconomic stability. Inflation closed 2025 at 5.4%, within the Bank of Ghana’s target band. The Monetary Policy Committee of the Bank of Ghana announced a 250 basis points cut to the policy rate to 15.50% on 28th January 2026. This is expected to improve real interest rate conditions and investor confidence. However, the scope for further declines in Treasury bill rates is constrained by fiscal and supply-side dynamics. The 2026 Budget projects a financing gap of about GH¢34.4 billion, to be funded largely from domestic sources, while weekly Treasury bill auctions and planned GH¢10 billion in infrastructure bond issuance will keep supply elevated.

As a result, further yield movements in 2026 following the expected immediate drops in T-bill rates will likely be driven more by supply-demand conditions than by further monetary policy easing. To frame these dynamics, Table 1 below presents three scenarios for the fixed-income market based on alternative assumptions around inflation, fiscal execution, and investor demand.

ECONOMIC AND MARKET OUTLOOK, AND STRATEGIC INVESTMENT ORIENTATION FOR 2026

9

Table 1: Fixed Income & Policy Rates Outlook – Scenario Table (2026)

ECONOMIC AND MARKET OUTLOOK, AND STRATEGIC INVESTMENT ORIENTATION FOR 2026

10

VII. Key Themes and MIIF’s Strategic Orientation

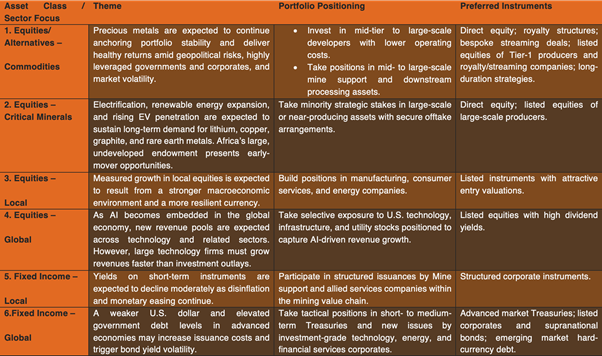

MIIF’s strategic orientation for 2026 is anchored on capturing opportunities arising from structural shifts in global markets while maintaining portfolio resilience amid macroeconomic and geopolitical uncertainties. The strategy emphasizes exposure to commodities and critical minerals to benefit from the energy transition and electrification trends, selective positioning in global and local equities to harness AI-driven growth and domestic recovery, and a balanced fixed income approach to manage yield volatility and liquidity conditions. Together, these themes support a diversified portfolio positioned to deliver stable long-term returns while managing downside risks across asset classes and regions.

Table 2: MIIF’s Strategic Investment Orientation

ECONOMIC AND MARKET OUTLOOK, AND STRATEGIC INVESTMENT ORIENTATION FOR 2026

11

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}